Time to Buy These E-Commerce Stocks as Amazon Potential customers the Way? – August 4, 2023

Pursuing Amazon’s (AMZN – Cost-free Report) ) amazing second-quarter benefits on Thursday, investing in e-commerce appears quite intriguing right now.

Quite a few Chinese e-commerce businesses also look eye-catching with Alibaba (BABA – Absolutely free Report) ) and JD.com (JD – Absolutely free Report) ) standing out in advance of their quarterly reviews later on in the thirty day period. Notably, the world-wide e-commerce sector is believed to be valued at upwards of $10 trillion dollars.

This makes investing amongst the big e-commerce players really lucrative as there is certainly probable for substantial gains in the potential. Even though the compound once-a-year expansion charge (CAGR) for the world-wide e-commerce industry has naturally slowed it’s continue to approximated to be about 10%.

Moreover, a 10% CAGR is interesting taking into consideration the size of some of the important e-commerce gamers like Alibaba and Amazon. Moreover, there are hidden gems in the worldwide e-commerce market with now seeking like a fantastic time to spend in the space.

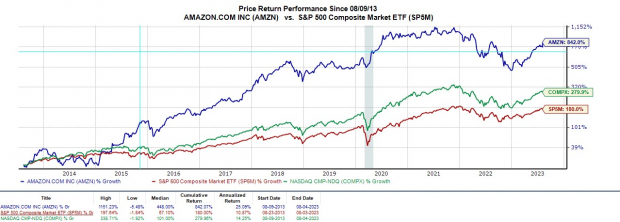

Impression Resource: Zacks Investment decision Analysis

Amazon’s Q2 Report

With inflation continuing to ease, Wall Avenue has been scoping out the development and outlook for massive tech companies during their quarterly studies and Amazon did not disappoint.

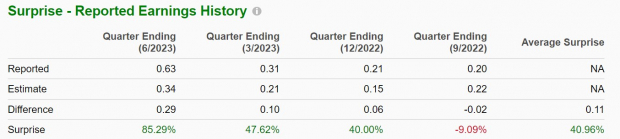

Amazon’s stock spiked soon after blasting Q2 earnings anticipations on Thursday, highlighting that income have been boosted by sturdy need for its numerous e-commerce goods and document shipping and delivery occasions. Earnings of $.63 for every share impressively topped Q2 EPS estimates of $.34 by 85% and soared 530% from earnings of $.10 a share in Q2 2022.

Graphic Resource: Zacks Investment decision Study

Astonishing a lot of analysts and delighting investors, Amazon seems to be prioritizing profits rather than expansion at the minute. To that point, Amazon’s web earnings for Q2 was a incredibly impressive $6.7 billion as opposed to a loss of -$2 billion in the prior-calendar year quarter.

Quarterly product sales of $134.38 billion beat Q2 anticipations by 2% and rose 11% from a 12 months back. Amazon’s dominance as an e-commerce company has permitted the corporation to develop into other spots and It is notable that Amazon Net Providers (AWS) profits were being up 12% with Advertising and marketing Companies revenue up 22%.

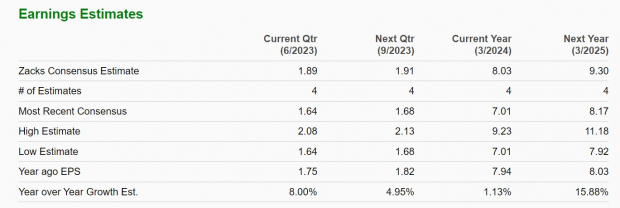

Amazon stock currently lands a Zacks Rank #3 (Hold) and a invest in rating could be on the way with Q2 success reconfirming a potent earnings outlook. Once-a-year earnings are now forecasted to skyrocket 118% in fiscal 2023 at $1.55 for each share compared to $.71 a share in 2022. Furthermore, FY24 earnings are expected to soar another 50% to $2.33 per share with it possible that EPS estimates will begin to rise.

Graphic Resource: Zacks Expense Exploration

Chinese E-Commerce

Alibaba and JD.com inventory glimpse attractive ahead of their quarterly stories on August 10 and 16 respectively.

Alibaba at present offers a Zacks Rank #1 (Strong Purchase) with JD’s stock sporting a Zacks Rank #2 (Acquire). The earnings outlook for equally of these Chinese e-commerce leaders is strengthening as logistics considerations subside subsequent the reopening of China’s financial system before in the year.

Alibaba’s fiscal first-quarter earnings are projected to increase 8% YoY to $1.89 for each share with profits predicted to be pretty much flat at $30.79 billion. Yearly earnings are expected to be up 1% in Alibaba’s present fiscal 2024 and climb an additional 16% in FY25 at $9.30 for every share.

Graphic Supply: Zacks Investment decision Investigation

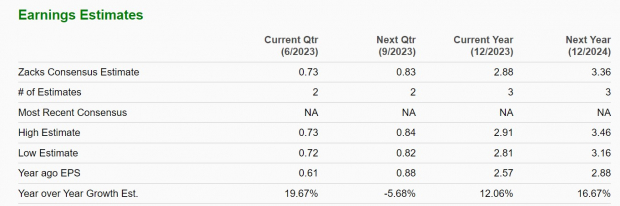

Pivoting to JD, its second-quarter earnings are predicted to leap 19% YoY to $.73 for every share even with profits forecasted to dip -2% to $39.25 billion. General, JD’s fiscal 2023 earnings are envisioned to bounce 12% with its base line projected to grow one more 16% in FY24 at $3.36 for each share.

Graphic Resource: Zacks Financial commitment Analysis

Hidden Gems

There are unquestionably e-commerce providers that are normally ignored for much more well-known names. On leading of that, providers like United Parcel Assistance (UPS – Cost-free Report) ) are significant to transportation, deliveries, and broader logistic factors.

UPS now lands a Zacks Rank #3 (Maintain) and will be a firm to hold an eye on when it reviews its 2nd-quarter benefits next Tuesday, August 8.

eBay (EBAY – Free of charge Report) ) is also a practical selection amongst e-commerce gamers and the business was capable to defeat its Q2 prime and base line expectations in late July. eBay has a Zacks Rank #3 (Keep) and may reward client investors with earnings anticipated to increase roughly 1% this 12 months and jump one more 9% in FY24 at $4.52 per share.

Bottom Line

It’s starting up to glance like an ideal time to invest in e-commerce companies. The outlook for many e-commerce players’ is strengthening and this must stay a viable space to invest in for 2023 and beyond.